Constellation Software: When Does a Stock Become a Bond?

When traditional equity frameworks begin to break down.

One of the most fundamental principles in finance is that stocks deserve higher discount rates than bonds.

The logic is straightforward. Bondholders have contractual claims on future cash flows while equity holders own whatever remains after everyone else has been paid. Most businesses face competition, disruption, recessions, changing customer preferences, technological change, and poor capital allocation decisions. Their future earnings are uncertain, and investors demand higher returns to compensate for that uncertainty.

Yet every so often, a company spends decades proving that its future cash flows are far more predictable and resilient than investors initially believed.

When that happens, investors start to discount those cash flows less like a stock and more like a bond. No company deserves a lower discount rate because management claims it does. It earns that privilege through decades of disciplined execution. Costco is perhaps the best modern example.

Today, investors willingly accept a free cash flow yield of just 2% because they have extraordinary confidence that Costco’s earnings ten years from now will be substantially higher than they are today. The market has gradually concluded that Costco’s risk profile is far lower than traditional equity frameworks would suggest.

That confidence did not appear overnight. It was earned through decades of consistent execution, customer loyalty, prudent management, and a culture that repeatedly made the right long-term decisions.

Charlie Munger at the 2022 DJCO AGM had a similar sentiment on why Costco shares were good investment (despite it trading at a 2% free cash flow yield at the time (and today too!)

“I would argue that, if I were investing money for some sovereign wealth fund or some pension fund, and I had a 30-, 40-, 50-year time horizon, I would buy Costco at the current price. I think it’s that strong an enterprise and that admirable a place... I think it has a good culture and a good moral ethos.”

I believe Constellation Software belongs in that same Costco like bond bucket (and with twice the growth rate in coupons).

Over the past six months, I have written extensively about why investors misunderstand the impact of artificial intelligence on vertical market software businesses. Rather than revisit those arguments here, I will simply state my conclusion: the market is dramatically overestimating the threat AI poses to many mission-critical VMS software providers.

That fear has helped create a valuation gap that is difficult to reconcile with reality.

The CSU Bond Case

At first glance, Constellation appears to be a software company.

In reality, it is a collection of more than 1,500 decentralized software businesses wrapped around one of the greatest capital allocation engines ever built.

Over the last three decades, Constellation has assembled a portfolio serving municipalities, hospitals, school systems, utilities, financial institutions, construction companies, transit authorities, and countless other niche industries around the world. These are not consumer applications competing for attention. They are deeply embedded operational systems, with private data, and decades long relationships with organizations rely upon every day to function.

The remarkable thing about Constellation’s portfolio is not any individual software asset. It is the diversification.

No single subsidiary drives the investment case. No single customer determines the company’s future. No single industry matters very much. Investors are underwriting a highly diversified collection of mission-critical software businesses spread across hundreds of end markets and thousands of customers. The resulting cash-flow stream is remarkably resilient.

Yet the software portfolio only explains where Constellation is today. It does not explain why it may still be compounding capital decades from now.

Culture Is The Ultimate Moat

To understand that, you have to study the culture.

Costco co-founder Jim Sinegal famously declared that corporate culture is “not the most important thing, it’s the only thing.” The companies that compound value for decades rarely do so because of a product. They do so because they build cultures that continue making intelligent decisions long after the founders have stepped aside.

The businesses matter, but culture determines what happens after the cash arrives. One of the most striking takeaways from CSU’s AGM was how deeply ownership remains embedded throughout the organization.Mark Miller, who was recently promoted to President, declined all compensation associated with the role.

Think about how unusual that is.

Promotions are always accompanied by larger salaries, larger bonuses, and richer equity awards. And at Constellation, one of the company’s most senior leaders accepted a promotion and got rid of his entire comp package. Miller already owns a substantial amount of Constellation stock. His financial future is tied far more closely to long-term per-share value creation than to a salary increase; but it’s the signal that matters.

That mindset traces directly back to Mark Leonard’s founding philosophy, where capital discipline and owner-operator thinking were embedded into the organization from the outset. Over time, that philosophy evolved into explicit norms around how shareholder capital is used internally; not just in acquisitions, but in everyday expense behaviour.

Even travel policy reflects that framing. Business-class travel is not treated as an automatic corporate entitlement, and in cases where employees choose to travel above the standard approved level, the incremental cost is paid personally rather than charged to the company. The intent is consistent rather than punitive: ensure that convenience and status do not become implicit claims on shareholder capital.

The signal is simple but insanely strict for a public company: comfort is optional, but capital is not to be casually consumed. Employees who earn performance bonuses are expected to reinvest 75% of their after-tax bonus proceeds into Constellation shares purchased in the open market. Those shares must then be held for a minimum of four years.

FCF Machine

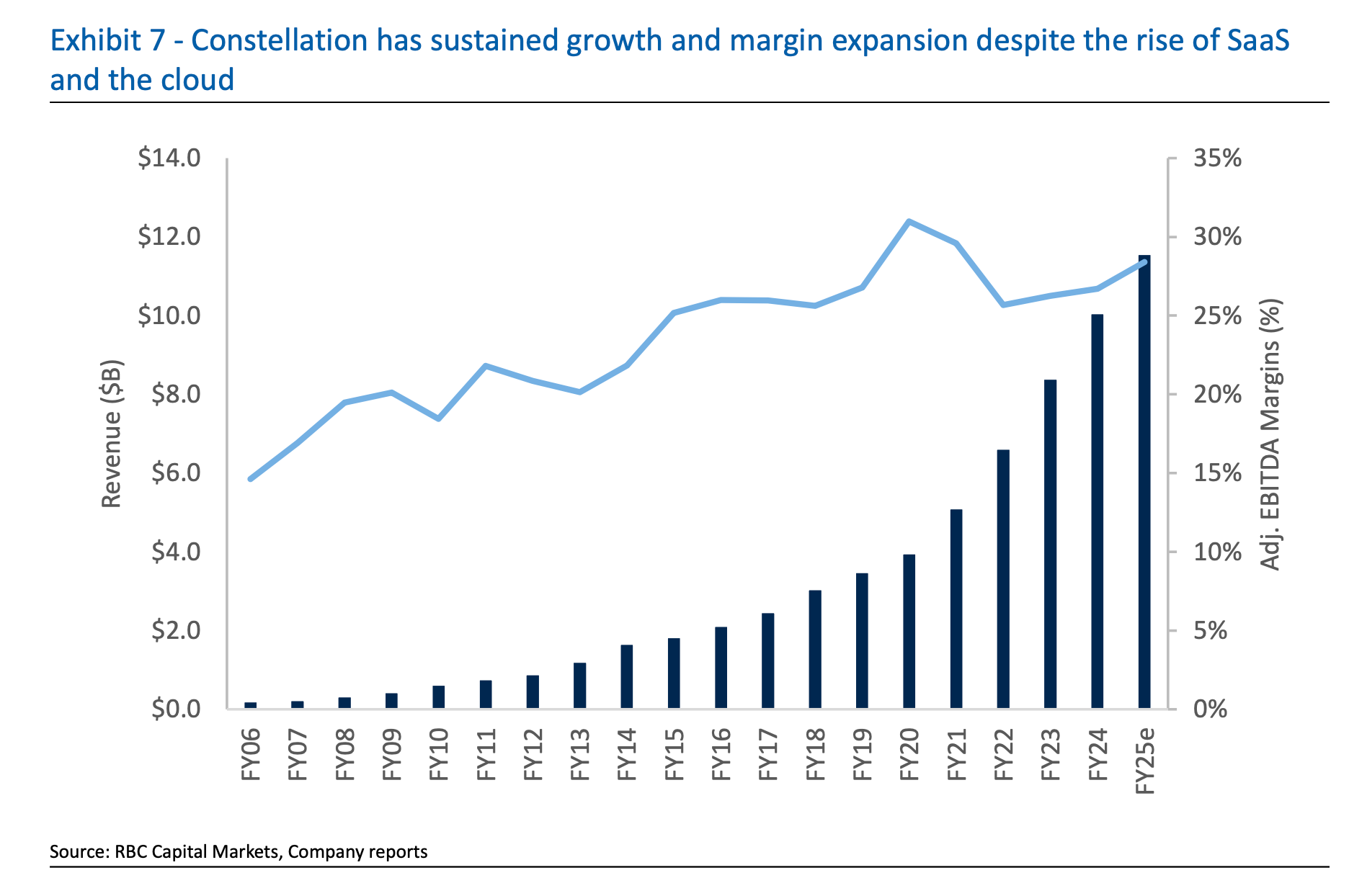

Over the last twenty years, Constellation has compounded free cash flow to equity per share at 26% annually while growing revenue per share at 24% with incredibility steady profitability. In fact, the company is anti-fragile with bad economic times allowing for more acquisition opportunities. Even in the midst of the GFC in 2008, Constellation had revenue explode higher by 36% (with organic growth of 5%).

Those figures are remarkable on their own. What makes them exceptional is how they were achieved. This was not a story of aggressive leverage, serial equity issuance or financial engineering. Constellation built its record the old-fashioned way: generating cash from existing operations and reinvesting that cash into additional high-return opportunities.

The compounding has continued through multiple technological changes: Through the internet, cloud, mobile and now AI, each technological shift looked existential in real time. Constellation simply adapted, embraced change and continued allocating capital. Ironically, the biggest challenge Constellation faced over the last several years was not AI.

It was excessive optimism.

For much of the past decade, software stopped being viewed primarily as an operating business and started being viewed as a financial asset. Cheap capital flooded the industry, private equity firms raised enormous funds, and acquisition multiples expanded dramatically.

For a company whose success depends on disciplined capital allocation, this created a genuine headwind.

Constellation refused to abandon its return hurdles. While competitors paid increasingly aggressive prices, management largely maintained the discipline that had made the company successful in the first place.

As acquisition opportunities became scarcer, growth naturally slowed. Many investors interpreted this as evidence that Constellation’s best years were behind it. I believe they misdiagnosed the problem. Constellation did not lose its edge, the acquirers just became irrational. Software assets simply became too expensive and Constellation stayed disciplined.

Post pandemic, investors have treated Constellation’s slowing acquisition growth as evidence that the company’s best days are behind it (RBC estimates 17% FCF growth over the next 3 years which is below its historical levels).

However, the competitive dynamic is finally reversing.

Software private equity is sitting on an aging inventory of assets, with nearly 900 of roughly 3,250 active portfolio companies held for five years or longer. Many of the remainder were acquired during the 2020-2021 zero-rate era at valuations that increasingly look difficult to justify.

Those investments eventually need to be sold. Limited partners want liquidity and fund lives are finite. The buyers willing to pay 2021 prices have largely disappeared.

Earlier this month, a Constellation executive summarized the opportunity perfectly:

“The speculative era where software companies commanded unjustifiable valuations is coming to an end. This opens up a fantastic window of opportunity for us to acquire great, sustainable businesses that might have previously opted for short-term financial buyers.”

In the first 5 months of the year CSU has deployed more capital than in all of 2025.

Yet despite this backdrop, the market continues to value the company as though growth is disappearing. Or perhaps AI fears are still the biggest drag…

AI Disrupting VMS Argument Looms But Is Losing Steam

In 2026, most investors hear the phrase software company and immediately think about technological disruption, competitive threats, and uncertain cash flows. That framework makes sense for some software companies, but definitely not VMS providers. Again, I have written extensively on this but here is a quick recap.

“When software costs are this small, the potential savings from switching are modest, while the operational risk of replacing a trusted provider is high… AI is often framed as an existential threat to software incumbents, but in vertical markets, it may be a source of advantage instead. Topicus has described AI as enabling a new layer of software that sits on top of existing systems to automate tasks and improve workflows.”

Or as other substackers highlighted:

"Code is not the hard part. Selling software to a risk-averse institution, passing security/compliance reviews, integrating with legacy systems, training staff, and earning enough trust to become deeply embedded in workflows. That’s the hard part." - NikNotes

“CSU is using AI to lower its own internal costs, i.e. faster deployment cycles, automated support resolution, compressed testing timelines, … while simultaneously using the productivity gains to invest more deeply in customer intimacy rather than extracting them as margin.” - ExpanseStocks

The companies that already own the customer relationship and control the data are often in the best position to layer AI-driven functionality on top of existing products.

AI is creating new opportunities for trusted system-of-record providers.That is precisely the assets Constellation can offer. The market seems to be slowly coming around with CSU shares rallying 24% in less than a month. Even the AI disruption leaders shifted from the disruption fear.

Andrej Karpathy, who popularized the term “vibe coding,” has largely moved on from it, in favor of what he now calls “agentic engineering”, (which is exactly what CSU is perusing for its customers).

Is CSU A Bond?

In terms of long term income reliability? Yes, I believe it is.

But it’s better than a bond in every way. Bonds pay fixed coupons. CSU has bond like safety but with a higher yield and high growth coupons.

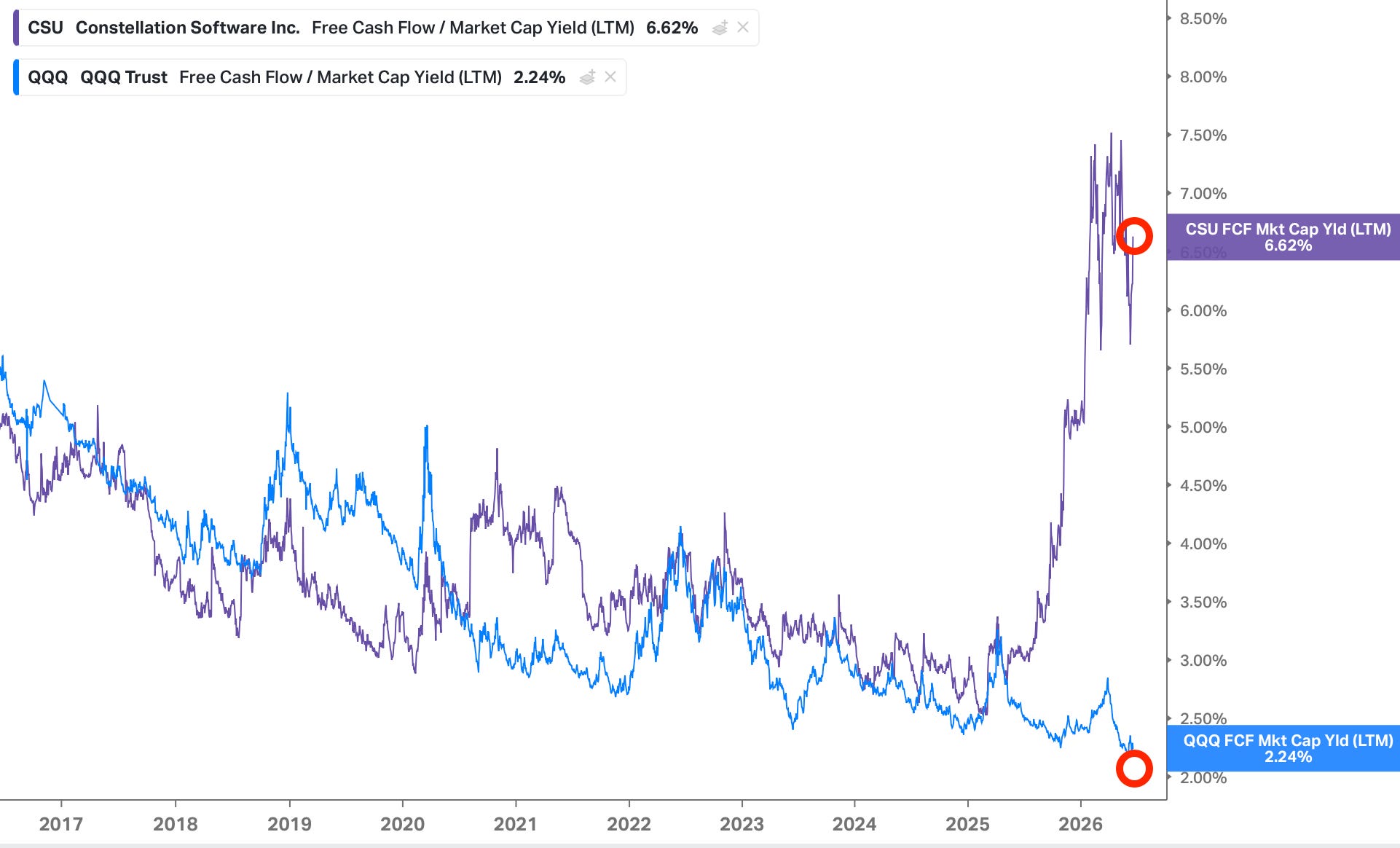

Today, investors can purchase that fast growing coupon at a 6% free cash flow yield, substantially higher than the 4% U.S. Treasury (which will never grow) and more than three times the 2% yield available in the average large-cap technology company (ironically the same as Costco these days due to the AI capex boom).

Investors continue to discount Constellation’s future cash flows as though they belong to an ordinary software company when decades of evidence suggest they are substantially more predictable than that.

This is ultimately what the market is missing. Investors are using the wrong discount rate. What’s the right discount rate?

If you use the US 10 year, then CSU is worth $4,100. However, the 10 year assumes zero growth in earnings. If you use Costco’s FCF multiple (which only has half the expected growth as CSU), then CSU is worth $9,000.

I don’t know the right discount rate but I do know it’s lower than the $2900 share price it is currently implying.

Valuing a stock like a bond is a risky prospect as 99% of companies will not live up to the safety that bonds offer. However, I believe that years from now, investors will conclude that with CSU they were never buying a generic software provider. They were actually buying a high growth bond, at a price that assumed it would never grow again. CSU has the right culture, track record and valuation that makes it a punch card opportunity.

Hi Trevor, great piece and fully agree with all points. I think the 6.2% yield is misleading though as based on their LTM Q1-26 FCFA2S, it's closer to 4.3%?

Great Article. Regarding AI, it means that more problems are now profitably solvable using software. Therefore, Constellation should see more opportunities to extend the value proposition of each of their businesses.

Regarding bonds, Despite the academic theory that they are less risky than stocks, that only holds up over relatively short periods. For the long run they are actually more risky due to inflation and interest rate risk. Remember those fixed coupons lose purchasing power every year.

Finally, have a look at Roper, they are similar to Constellation, in fact Mark Leonard used them as a benchmark in one of his letters