Short Attacks and Tobacco Stocks

$FFH.to $BTI

What a crazy start to February.

We finally get our BAT article into the Globe and then boom Muddy Waters comes out with a short attack on Fairfax. Less than 3 hours later I’m doing my first National TV appearance. I stumbled on some words, forgot to smile and I should have leaned into some key points but it went pretty well.

My theory for going on air was that even if I had a fairly bad interview, the short report from Muddy Waters was so weak that my response would age well from just being right. The potential client inquiries alone have been worth it actually. People like seeing a real person behind the words it seems!

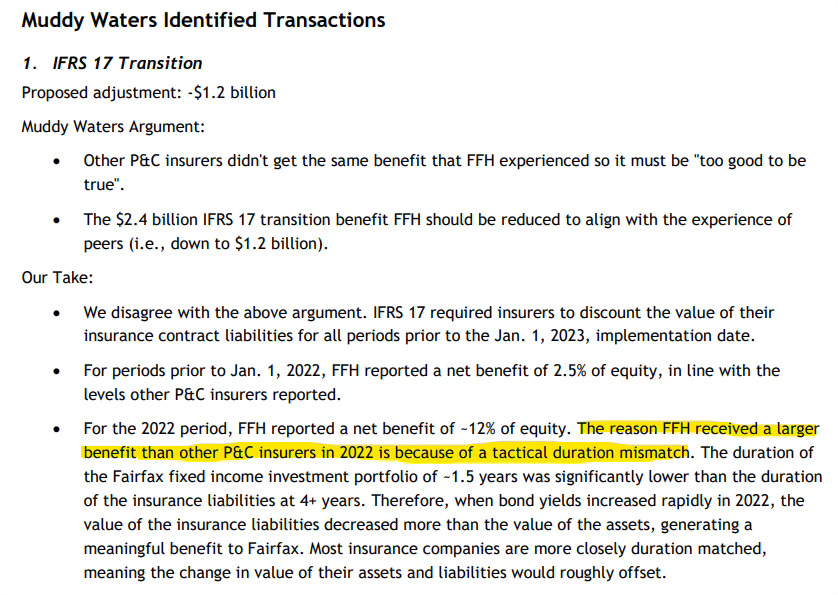

I honestly have no idea how people took this Muddy Waters attack seriously. The two major accounting points are the transition to IFRS 17 and Digit’s valuation. IFRS 17 was a mandated change that increased Fairfax’s book value that Muddy Waters used as proof that the company was aggressively trying to overstate equity. The reality is that Fairfax has a long history of conservatively estimating its reserves which had to be rolled back with IFRS 17. In addition, as a long tail insurer Fairfax had more to gain from the discounting and duration effect that took place under the accounting transition than the short tail peers cited.

The second claim is that Digit is grossly overvalued and Muddy Waters implied that Fairfax had used internal estimates as the basis for its carrying value. This is untrue as a third party investor, Sequoia Capital, had invested in its latest round and that was used to mark the asset. They also claimed that this valuation was now grossly overstated based on publicly traded peers which had fallen since that funding round. Digit is a significantly more profitable company than the peers Muddy Waters cited and Digit never achieved the lofty valuation levels that occurred in public markets after the pandemic.

The report also conveniently ignores the many instances where Fairfax has actually understated its asset values such as with Fairfax’s pet insurance division which it sold in 2022 for $1.4b, 7x its reported book value. In addition, investments like Eurobank which are hundreds of millions above its current carrying value. Just ignore those facts eh? Sure, the Odyssey and Brit transactions in 2021 did free up capital and slightly increase book value but these deals were just acknowledging the economic value of the divisions that were understated on Fairfax’s balance sheet.

The point I pushed in the interview really nails it, the bear case from the MW report is that Fairfax’s book value is overstated by 18%.

Even if that were true (and again, we disagree completely on their claims) it would not materially affect the company’s value or trajectory. They never questioned the billions of dollars from interest and underwriting profits that are powering the company forward (and have been locked in for 3 years).

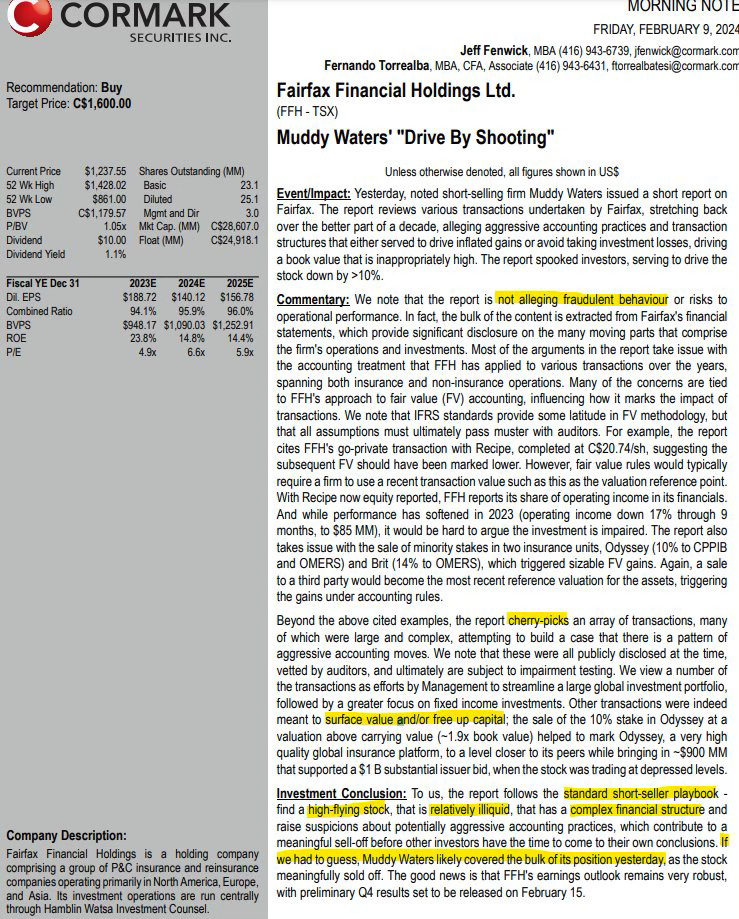

I’m not anti-short seller, I think they are critical to well functioning capital markets but this is really just a smash and grab or as Cormark called it, ‘a drive by shooting’. MW are trying to capitalize on the run up in shares and went on this huge media tour right before Fairfax releases earnings so they can’t respond due to their quiet period.

Muddy Waters has done some excellent work but this is very clearly empty. The stock fell around 14% at its lowest so MW probably did make a very large, quick profit but this will certainly hurt their reputation moving forward.

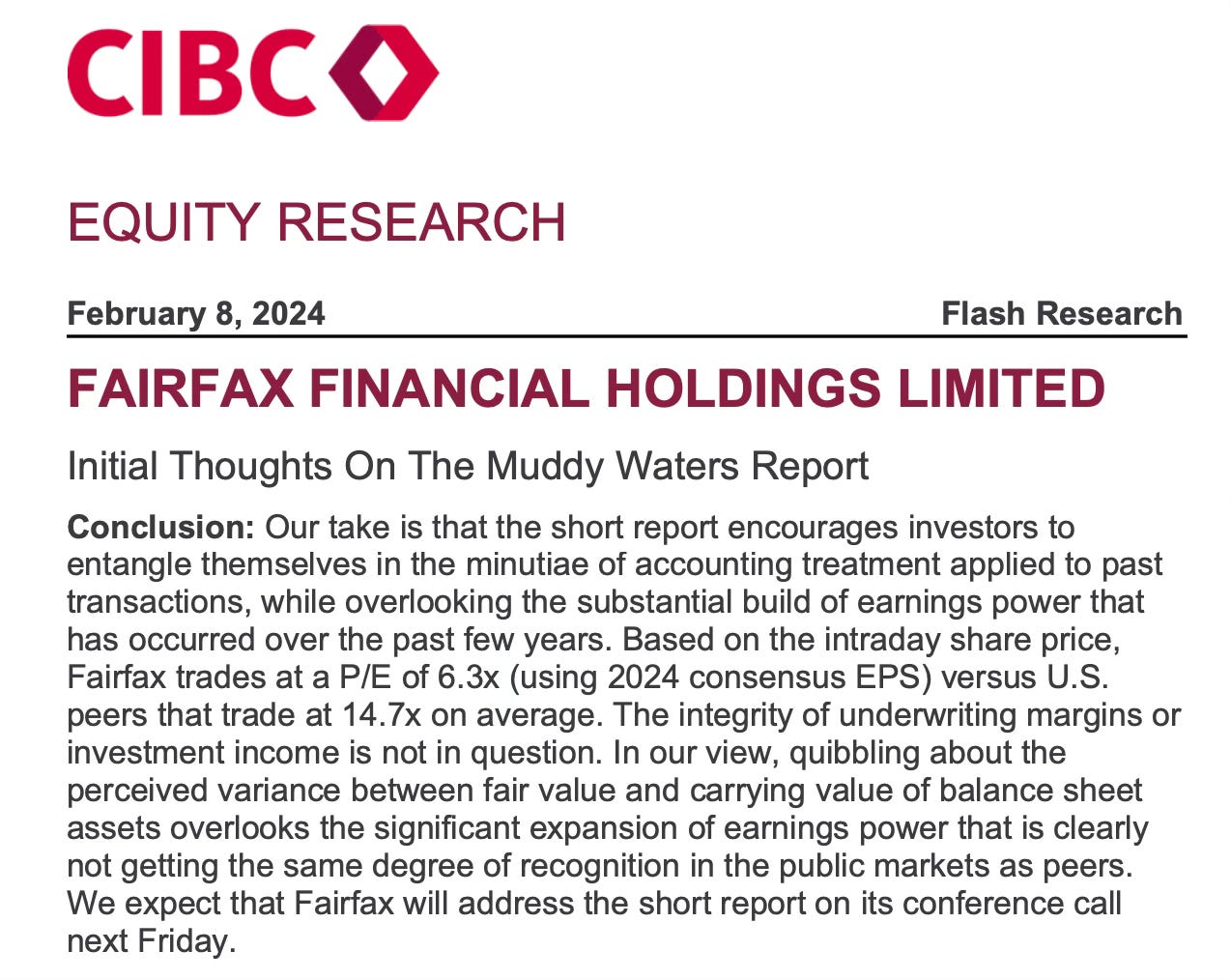

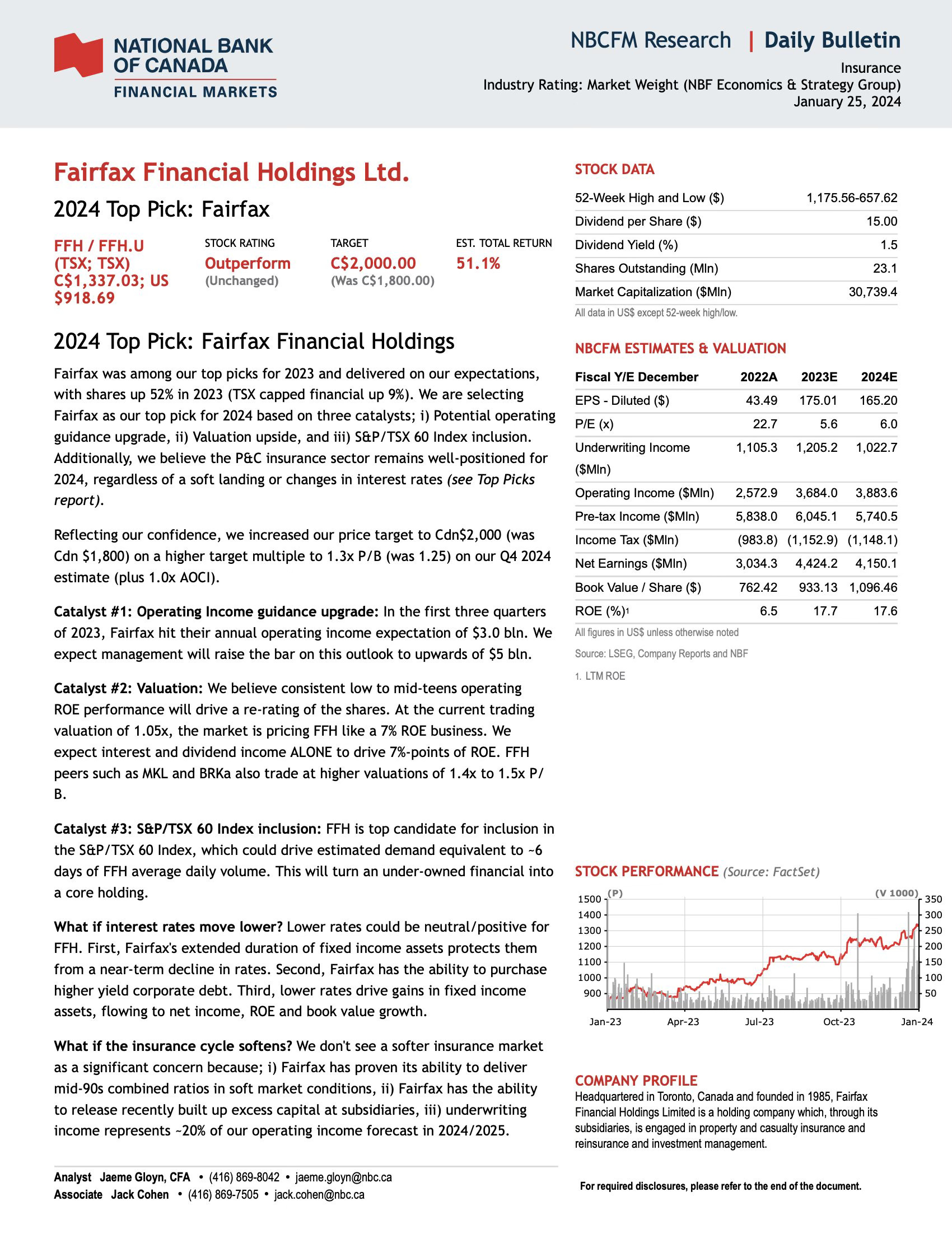

The broker reports from Bay Street have been coming out pretty fast and reaching similar conclusions. (I’ve attached some screen shots below).

At the end of the day, Fairfax trades at book value, 5x earnings and duration now locked in for 3 years. With Prem having nailed the timing on interest rates, it’s arguably cheaper today than it was 2 or 3 years ago. The company still trades at a massive discount to its peers and its equity portfolio is filled with cheap value stocks and high quality government bonds. It’s encouraging to see Bay Street start to come around (I attached the cover of National Bank’s recent top pick report below).

I bet MW has already covered their short or will early this week.

The BAT thesis is that although smoking is clearly on its way out, nicotine is a secular grower. The most notable company is Philip Morris with its less harmful next generation of products like IQOS heat not burn that is finally coming to the US and Zyn oral pouches that are spreading like wild fire. So why BAT over PM? Valuation.

When you want to get long a sector and you think sentiment is going to shift, get the cheapest company, not the best. It’s similar to playing oil in the pandemic when WTI went negative. I foolishly went for the safest play in Prairie Sky (a royalty co with a great balance sheet) when the correct call (if you believed the sector was cheap) was to go long the weaker juniors that had a ton of sensitivity to an oil rebound.

BAT has been left for dead and is actually sitting on some great next gen brands (Velo) and by far and away the number one vape brand (Vuse, 47% market share in legal channels), and it trades for 6x earnings (PM is 18x) an all time low and its leverage will finally hit its target next quarter.

Here is a PE chart from our Q4 client letter.

Yes a lot of the drop was due to the overpriced Reynolds acquisition and BTI has greater combustibles risk and menthol exposure, but the stock is cheap.

The idea has been floating around my head for a while and came from a trip to Miami. If you go into any one of these clubs, you’ll see that vapes are everywhere, there’s a whole new generation of nicotine users. Because the vapes don’t smell and almost never set off fire alarms, security doesn’t stop vaping indoors, it’s like the 1970s was with smoking. I’ve actually had some friends vape at my place without asking me if they can do it inside. Is that rude? Yes. Does it make me bullish on nicotine usage? Absolutely.

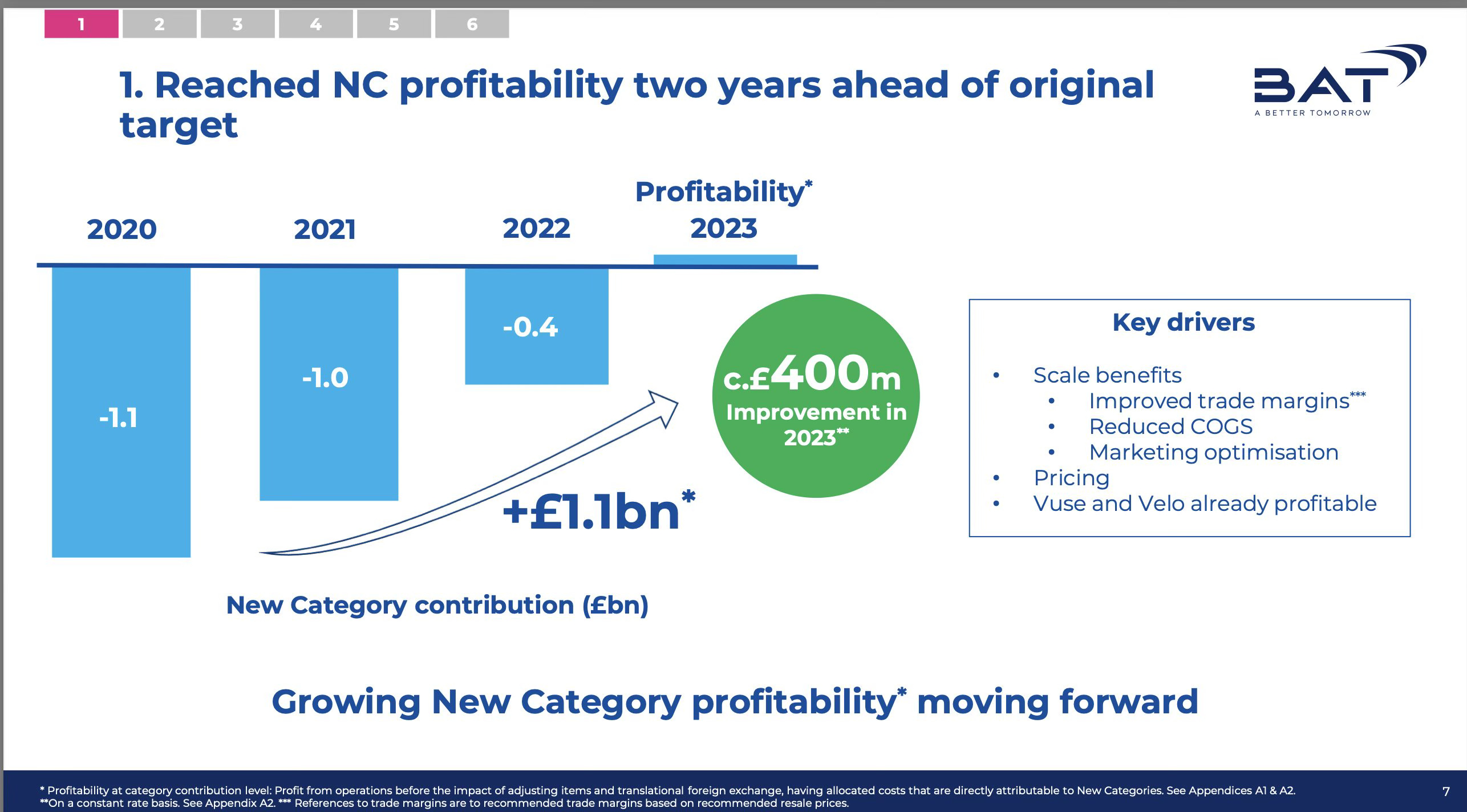

Since most of the US vape market is illicit Chinese disposables (60%), the actual benefit to big tobacco is limited and they are fighting with hands tied behind their back but it appears to finally be getting under control (see the article). The recent regulator crackdowns are what finally caused me to buy in. Even without regulators getting their act together, BAT’s next gen division is already profitable, 2 years ahead of schedule, from a 1.1bn pound loss in 2020.

As investors figure out that these less harmful, next gen products are the future, the stocks should rerate. Even today many investors are surprised to learn that the financial results are so strong. From 2018 to 2022 at BAT adjusted earnings per share increased from 297 pence to 371 pence (even with the majority of profits being paid out as dividends). These tobacco stocks pump out cash (almost zero capex), the buybacks will heat up this year.

I know everybody thinks we will never have a recession again but I do enjoy being in a stock that is seen as defensive. I mean it already has a well covered 10% dividend yield, how cheap will it really get from here? Honestly, you could make an argument that you should want the stock to stay cheap and just buyback shares, investors could do well in either scenario at this valuation. Or maybe I just love buying companies that are highly out of favor. We shall see.

The S&P has been up 12 of 13 weeks and now everybody is bullish. I just watched an interview with Steve Eisman of The Big Short fame saying he’s not even concerned because the US consumer is in such good shape and he only goes long now. Wow, that’s interesting… I’m not going to even attempt to say where the market is headed (that’s a fools errand and not a long term strategy) but I’m not seeing a ton of value in the big names that everybody else loves and I’m certainly not going to start chasing Nvidia at 95x earnings just to keep up.

With the S&P at 25x trailing earnings and some of our disclosed stocks like Fairfax at 5x and BTI at 6x (4x ex-ITC), a bunch of obscure value stocks, M&A, and some tactical put options, our fund’s returns should be more uncorrelated to the markets than it normally is. That would scare the majority of fund managers due to the high tracking risk but it’s music to my ears. As Sir John Templeton said “If you want to have a better performance than the crowd, you must do things differently from the crowd.”

Anyways, I hope everybody has had a wonderful 2024 so far and I’ll try and write more often. I just need to see some more deals!

Trevor

NBF

National Bank Write Up (Jan 25, 2024)

Great write up. Happy to receive those more often.

Reg. "They never questioned the billions of dollars from interest and underwriting profits that are powering the company forward (and have been locked in for 3 years)."

> 1st part is true: MW did not question it, maybe coming in 2nd report, aka attacking in waves

> 2nd part: underwriting profits are never locked in I guess bc future UW profits (per Definition) depend on claims which are at least partially driven by probability. Interest rates might be locked in but some ob the fixed income instruments clearly come with credit risk, which most likely are fine, but nothing is locked in. The game is not over until it is over.