This year we moved to sharing our quarterly partner letters on a one quarter delay.

Our Q4 letter (link) discusses British American Tobacco.

Since this letter, the immediate ban on the sale of menthol cigarettes has been removed which was one of the biggest risks to near term earnings.

Tobacco stocks have been getting a bit hot recently due to the explosive growth of nicotine pouches which runs counter to the narrative of the death of big tobacco (spoiler alert: It’s big nicotine, not big tobacco and they aren’t going anywhere). We also presented the idea at the YYZ Stock Pitch Competition in April and won alongside the Terravest pitch from Chris Waller of Plural Investing.

Here is an audio file of the presentation if you are keen on hearing an old value guy like myself have a little fun.

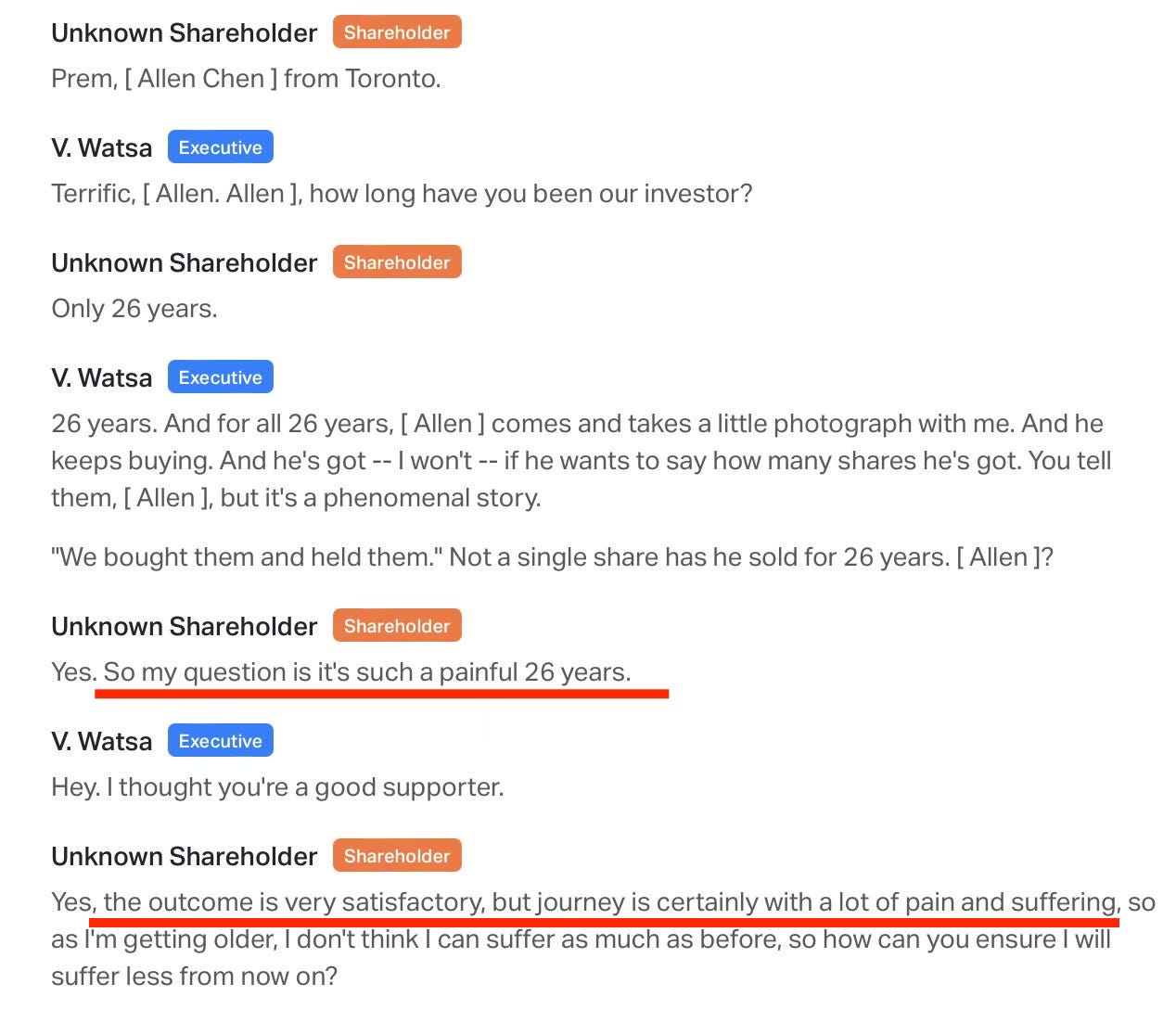

I attended the Cymbria investor day yesterday, they are the only institutional investors that ever understood the transformation at Fairfax. It was a great event, their idea they presented? Still Fairfax! The stock has 3x’d since covid but has transformed so much that it is just sitting there today at book value and 7x earnings with 3 years duration locked in. Cymbria talked about how bias can impact investors and they had this great video of Alan Chan, a shareholder for 26 years, at the most recent AGM. I think Prem would be displeased if I shared it publicly so I’ll just do the transcript.

Alan Chan is a legend and a great friend of the Toronto investing community, I really should do a post on him one day….

What Cymbria was saying is that if a shareholder who has done well on the stock over 26 years has so much distress from holding the investment, can you imagine how hard it would be for a PM that has previously lost money on the stock to buy back in?

I think you will see Bay St really come around when it gets closer to an S&P/TSX 60 inclusion which seems increasingly likely with every quarter.

The cherry on top yesterday was Berkshire revealing their mystery stock was Chubb Insurance. Here’s what I wrote on twitter (X).

Viking had similar thoughts

The quick line of thinking is that if Berkshire likes Chubb at 1.7x book, then they would love Fairfax at 1.1x book, it has way better returns and prospects too.

The Digit IPO is just about to occur, again this is a private insurer in India that Fairfax helped start, Muddy Waters said at best it was going to be worth $1.5bn and this was the biggest part of their short thesis. Of course, Fairfax was right and it’s pricing at $3bn (It’s a tight float so it wouldn’t surprise me if it rips higher on its first day). I don’t know what MW was thinking shorting Fairfax, but I thank them for their service of letting me add a bunch of shares in the C$1200s. FYI MW’s bear thesis on Blackstone Mortgage Trust ($BXMT) makes total sense to me.

So, I could keep rambling about stuff like how I think that office NAVs are a big ponzi scheme and the whole sector will blow up or how stocks like Duolingo, Wingstop and Coinbase are priced to perfection but that’s just me venting.

The market’s not cheap, credit spreads are way too tight. I’m finding value in low multiple uncyclical companies, I’m sure some people are frustrated we are not in Nvidia and the AI stocks, and I understand that but I don’t think it’s a great investment opportunity at today’s prices. I love our portfolio of companies, they’re minting cash flow. We are doing work on a new name that looks very attractive with no economic correlation, hopefully it makes it in.

Talk soon,

Trevor

You made me look up the 26-year CAGR of FFH: 5.8%. Now I'm sure he bought a bunch of shares when the price was much lower than 26 years ago and so had a much better return, so I'm not saying that's his return, but looking at the chart, I can certainly see why it was painful for long periods!