Is Apple An Above Average Business?

Apple, the most well covered stock in history appears cheap.

Everybody knows this company so let’s just jump to what I think the market is missing.

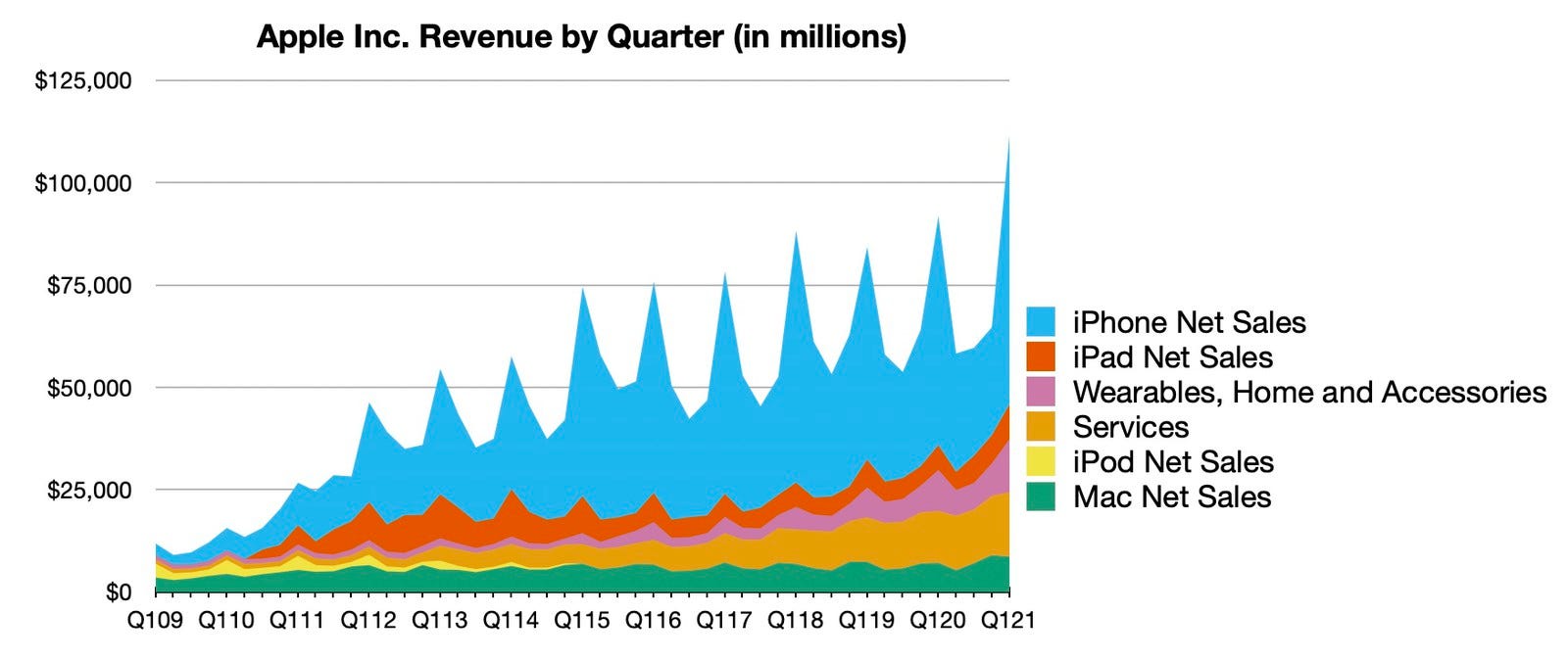

Apple’s Ecosystem: What is under-appreciated is not the existence of the Apple ecosystem but the extent of its growth in the past decade.

An iPhone user in 2011 may have had an iPhone, iPad and Macbook.

An iPhone user in 2021 could very well have the above, plus an Apple Watch, AirPods, Apple TV and many recurring subscriptions (Apple Music, TV+, Arcades, News+, third party apps).

The more devices/subscriptions you have, the greater your lock in.

Apple’s moat is getting wider and I think it’s under-discussed.

Let’s frame it another way.

Think about when you bought an Apple device or received one as a gift.

What did you feel?

My guess is happy or excited.

Me too!

But the reality is you are also unknowingly getting dragged deeper into the Apple ecosystem.

The digital chains of habit are too light to be felt until they are too heavy to be broken.

Apple’s Silicon: 2007 is widely cited as a game changing year for Apple since Steve Jobs unveiled the iPhone. But it was also the first year that Apple developed its own system on a chip. Fast forward to today and Apple is doing things with its silicon that are blowing my mind.

For decades, Apple has relied on Intel for its Mac computer chips but in 2020, Apple began a two year transition that will bring its proprietary mobile chips into its computer line.

The initial results are incredible with near universal praise on performance and battery life, and furthers Apple control over its product development. (Expect to hear a lot more about Apple Macs in 2021. Their market share is going to explode.)

Only Apple with its integrated hardware/software approach can routinely pull off game changing devices. Apple’s W1 chip in 2016 allowed for instant bluetooth pairing on their AirPods that was described as ‘magical’. I expect the recently released AirTags that feature Apple’s U1 chip will garner similar fanfare.

So Apple’s a fantastic business with a great moat.

Everybody already knows this!

Well do they?

Here we are in 2021, and Apple is trading for 23x earnings (ex-cash). The exact same multiple as the S&P 500.

The market is still pricing Apple as an average business.

Even a high school student knows that Apple is an above average business.

Let’s frame it another way.

Coca-Cola trades at 25x earnings, McDonalds trades at 27x earnings.

Apple, a company that has revolutionized computing technology and has a lock on 1 billion plus high income consumers, is valued for less than sugar water and hamburger makers.

That makes zero sense to me.

Now let’s look at some the bear cases.

5G Supercycle: The bears will quickly point out that 2021’s earnings are ‘cyclically high due to the iPhone 12 being part of a supercycle.’

I call BS.

Other than tech nerds, nobody cares about 5G yet. Even the carriers are telling their customers to turn off 5G if they want better battery life instead.

People are buying iPhones simply because they love them and I don’t expect that to change anytime soon.

The same concerns happened in 2012 with the launch of the iPhone 5 that was the first Apple phone to have 4G.

Can you spot the much feared “4G supercycle?”

Neither can I.

Work From Home: Similarly, the bears will point out that the pandemic forced people to work from home and that brought forward demand.

Sure, there is likely an element of pull forward but that really doesn’t matter long term. Analysts have been obsessing on short term cyclical demand for years. They are missing the forest for the trees. The trend is relentlessly higher.

Implied Expectations:

Let’s look at how low the expectations are for the sell side estimates on Apple stock.

Analysts have Apple growing its topline at 3-4% per year for the next 2 years. This seems crazy low and is even less than the IMF’s global GDP growth rate.

I just can’t square that with what I’m seeing with consumers and businesses. Apple’s share of wallet is increasing every year yet the analysts still think that it will diminish?

Anyways, that’s a quick summary of my ‘Apple is an above average business’ thesis. We’ll see what happens.

Disclosure: Long Apple

This post is intended for informational purposes and should not be construed as an offering or the solicitation of an offer to purchase an interest in Tidefall Capital Management LP (the “Fund”). Past performance should not be mistaken for and should not be construed as an indicator of future performance and there is no assurance that the investment objectives of the Fund will be achieved. An investment in the Fund involves a high degree of risk. The information contained in this post is not, and should not be construed as, legal, accounting, investment or tax advice. The contents of this post are based upon sources of information believed to be reliable but no warranty or representation, expressed or implied, is given as to their accuracy or completeness. All opinions and estimates contained in this report constitute the Manager’s judgment as of the date of this report, are subject to change without notice and are provided in good faith but without legal responsibility. The Manager asserts that the reader is solely liable for their interpretation and use of any information contained in this post.